What is Bill Discounting?

Definition and Concept

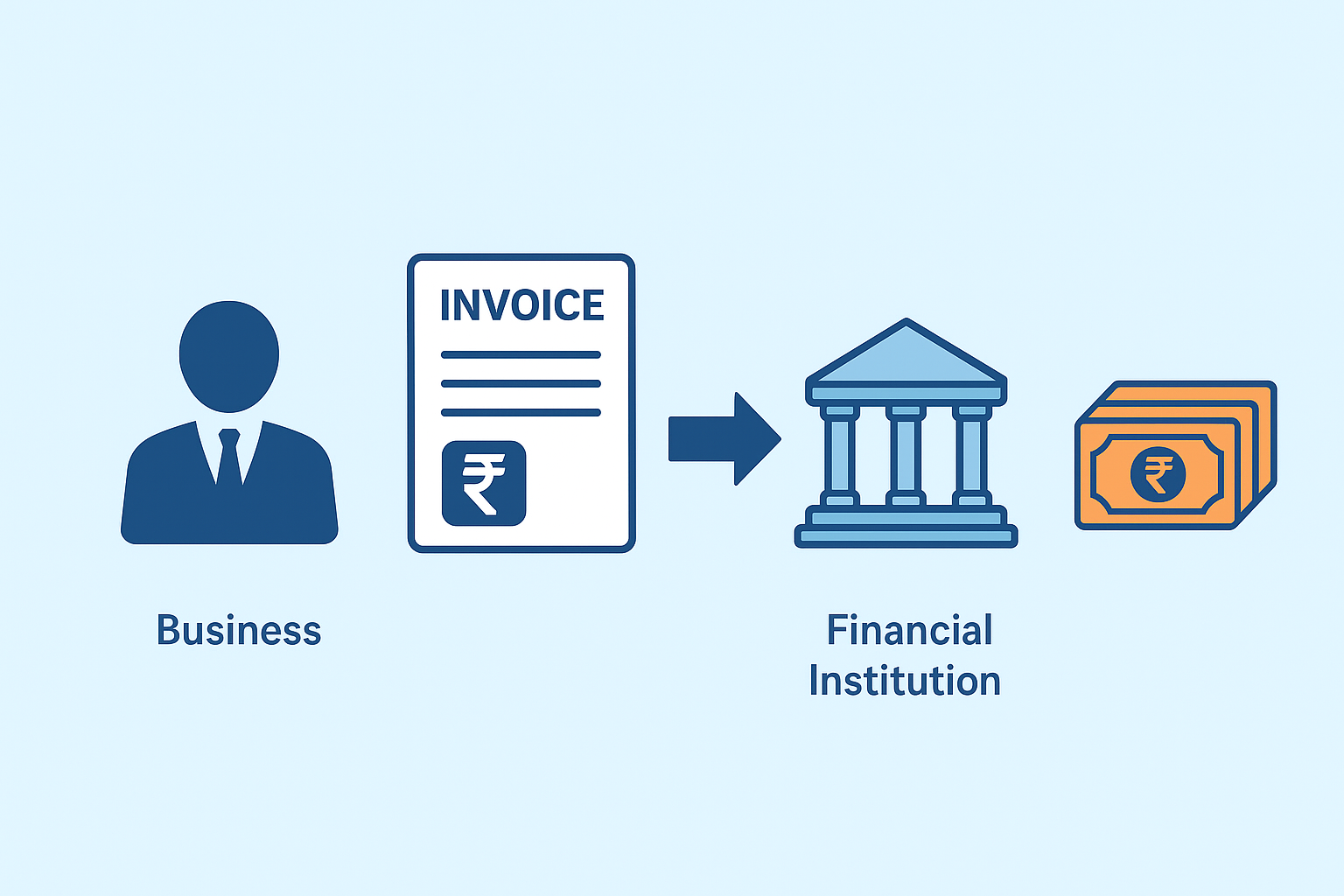

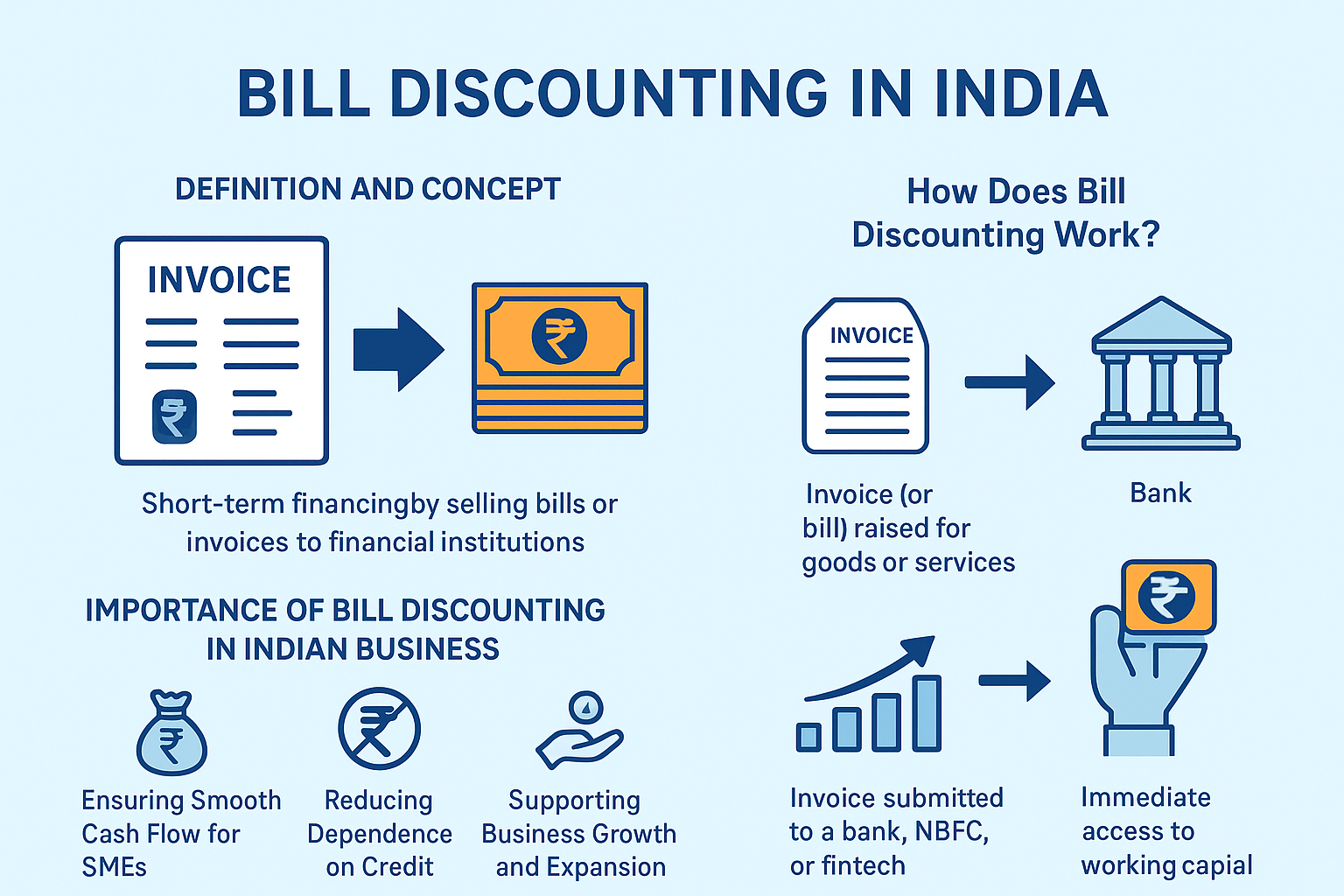

Bill Discounting is a short-term financing solution that allows businesses to get immediate cash by selling their trade receivables (bills or invoices) to banks, NBFCs, or fintech companies. Instead of waiting 30–90 days for customers to pay, businesses can convert receivables into instant working capital.

Difference Between Bill Discounting and Invoice Financing

While both involve receivables, bill discounting is typically used for trade bills backed by goods and services, whereas invoice financing is more flexible and often facilitated by fintech platforms.

Importance of Bill Discounting in Indian Business

Ensuring Smooth Cash Flow for SMEs

India’s SMEs often face delayed customer payments. invoice discounting ensures steady cash flow, helping businesses cover daily expenses like raw materials, salaries, and logistics.

Reducing Dependence on Credit

Instead of relying on high-interest loans or informal credit, SMEs can use invoice discounting to access funds at lower rates.

Supporting Business Growth and Expansion

Quick access to capital helps SMEs invest in growth opportunities, expand operations, and build credibility with suppliers.

How Does Bill Discounting Work?

Step-by-Step Process

- Business sells goods/services to a customer and raises an invoice.

- Instead of waiting for payment, the business submits the bill to a bank/NBFC/fintech.

- The lender verifies the bill and advances a percentage (usually 75–90%) of the invoice value.

- Once the customer pays, the lender deducts charges and releases the remaining balance.

Role of Banks, NBFCs, and Fintechs

- Banks: Offer bill discounting primarily to large corporates.

- NBFCs: More flexible for SMEs and mid-sized businesses.

- Fintechs: Platforms like KredX, M1xchange, and Invoicemart enable digital bill discounting with faster approvals.

Example of Bill Discounting in Practice

A textile exporter in Surat issues an invoice of ₹10 lakh with 60 days payment terms. Through a fintech, they receive ₹8.5 lakh immediately, ensuring uninterrupted operations.

Types of Bill Discounting in India

Invoice Discounting

Converting unpaid invoices into cash through NBFCs or fintech platforms.

Trade Receivables Discounting (TReDS)

An RBI-regulated platform (like RXIL, A.TReDS, M1xchange) where SMEs can discount bills with multiple financiers.

Supplier Bill Discounting

Suppliers get funds by discounting bills raised on large buyers.

Export Bill Discounting

Helps exporters receive payment before overseas buyers clear invoices.

Key Features of Bill Discounting

Short-Term Financing

: 30–120 daysCollateral-Free

: Based on receivables, not assetsQuick Access

: Faster than traditional loans

Advantages of Bill Discounting in India

Faster Cash Flow

No need to wait 90 days for customers—cash is available immediately.

Improved Business Credibility

Businesses gain credibility by paying suppliers and employees on time.

Growth Without Debt Overload

Unlike loans, invoice discounting doesn’t add long-term debt—it leverages existing receivables.

Risks and Limitations

Dependence on Customer Creditworthiness

: If the customer delays or defaults, risks increase.

Service Charges and Fees

: Processing fees can affect profit margins.

Limited Availability for High-Risk Businesses

: Not all SMEs qualify.

Bill Discounting vs. Traditional Business Loans

Factor | Bill Discounting | Business Loans |

| Approval Time | Few days | Weeks/Months |

| Interest Rate | 12–18% | 9–15% |

| Collateral | Not required | Often required |

| Repayment | Customer pays | Borrower repays |

Eligibility Criteria for Bill Discounting

Documents Required

- GST returns

- PAN, Aadhaar, KYC documents

- Business financial statements

- Valid invoices/bills

Business Turnover and Stability

Lenders prefer businesses with steady turnover and reliable clients.

Customer Credit History

Strong customer credit profiles increase approval chances.

Application Process in India

Applying Through Banks and NBFCs

Submit bills, KYC, and financial records for verification.

Fintech Platforms

Fast digital approval via platforms like KredX and M1xchange.

Role of RBI-Approved TReDS Platforms

Enable competitive bidding by multiple financiers, ensuring better rates for SMEs.

Alternatives to Bill Discounting

Overdraft Facilities

Business Lines of Credit

Invoice Factoring

Best Practices for Businesses

Choose the Right Platform

(Bank, NBFC, Fintech, or TReDS)

Maintain Customer Relations

to ensure invoice authenticity

Calculate True Costs

including discounting charges

Case Studies of Bill Discounting in India

SME Textile Exporter in Surat

Used TReDS to secure ₹50 lakh funding for export orders.

Startup in Bengaluru

Leveraged fintech platforms for payroll during fundraising delays.

Manufacturing Firm in Pune

short-term working capital solution worth ₹2 crore to fund raw material purchases.

Future of Bill Discounting in India

Digital Growth

: Fintech adoption is booming.Government Push

: RBI’s TReDS platform is expanding reach.SME Adoption

: More SMEs will use bill discounting for growth.

FAQs on Bill Discounting in India

1. What is the interest rate for bill discounting in India?

Usually 12–18% annually, depending on the platform.

2. Is bill discounting the same as factoring?

No. In factoring, the financier manages collections, while in discounting, the business remains responsible.

3. Can startups use bill discounting?

Yes, if they have invoices from reliable clients.

4. Which fintechs offer bill discounting in India?

KredX, M1xchange, RXIL, Invoicemart, and Oxyzo.

5. Is collateral required?

Generally no, since receivables act as security.

6. Who regulates bill discounting in India?

RBI regulates bill discounting via the TReDS framework.

Conclusion: Is Bill Discounting the Right Choice for Your Business?

Bill Discounting in India is a game-changer for SMEs, startups, and exporters struggling with delayed customer payments. By converting invoices into cash, businesses can maintain liquidity, pay suppliers, and grow faster.

With RBI pushing TReDS adoption and fintechs making discounting seamless, the future looks promising. For businesses seeking quick, collateral-free working capital, bill discounting is one of the best solutions.

👉 For more, visit the Reserve Bank of India (RBI) and TReDS platforms.