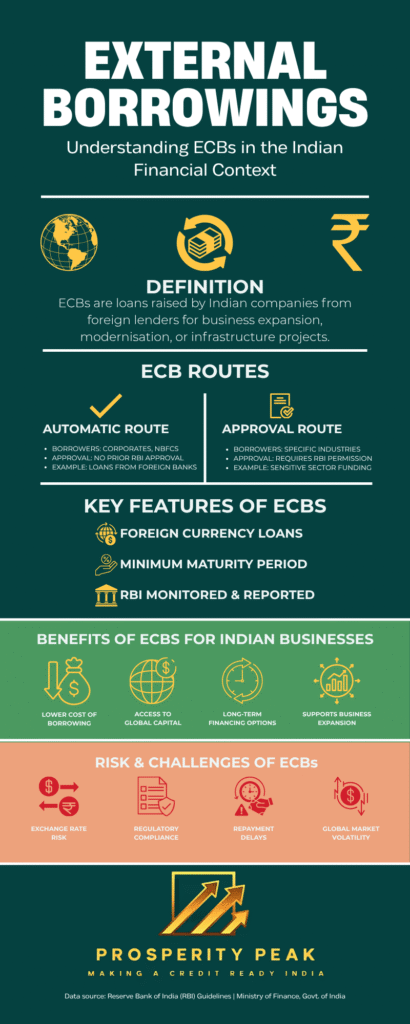

Introduction to External Commercial Borrowings (ECBs)

In a globalized economy, External Commercial Borrowings (ECBs) have emerged as a major source of financing for Indian corporates. They allow Indian entities to raise capital from foreign lenders, typically in foreign currency, to fund expansion, infrastructure, or other permitted business activities.

As India continues to integrate with international financial markets, ECBs have become a strategic tool for accessing low-cost global funds while reducing reliance on domestic borrowing.

What Are External Commercial Borrowings?

External Commercial Borrowings refer to loans availed by Indian entities from non-resident lenders, in the form of bank loans, buyers’ credit, suppliers’ credit, or securitized instruments.

These borrowings are regulated by the Reserve Bank of India (RBI) under the Foreign Exchange Management Act (FEMA), 1999, ensuring that inflows remain within permissible limits.

Why ECBs Matter for India’s Economic Growth

ECBs provide Indian companies access to global capital markets, enabling long-term funding for large-scale projects in infrastructure, manufacturing, and renewable energy.

They also diversify funding sources, reduce borrowing costs, and enhance competitiveness by offering favorable interest rates compared to domestic credit.

Regulatory Framework Governing ECBs in India

Role of the Reserve Bank of India (RBI)

RBI is the apex regulator overseeing all ECB transactions, ensuring compliance with monetary stability and external debt sustainability.

FEMA Guidelines and Policy Framework

Under FEMA, the ECB policy is periodically reviewed to maintain balance between capital inflows and currency stability.

RBI Master Directions and Reporting Requirements

Borrowers must adhere to the RBI Master Direction – External Commercial Borrowings, Trade Credits, and Structured Obligations (2019, updated). They are also required to report ECB transactions via Form ECB within 7 days of drawdown.

Types of External Commercial Borrowings (ECBs)

Automatic Route

No prior RBI approval needed; borrowers must meet eligibility criteria and sectoral limits.

Approval Route

Requires explicit RBI approval, often used for sensitive sectors or complex structures.

Track I, Track II, and Track III

Track I: Medium-term foreign currency-denominated ECBs (3–5 years).

Track II: Long-term foreign currency ECBs (10 years+).

Track III: Rupee-denominated ECBs (Masala Bonds).

Eligible Borrowers and Recognized Lenders

Who Can Borrow?

Eligible borrowers include:

Indian corporates in manufacturing or infrastructure

NBFCs and housing finance companies

Public sector undertakings (PSUs)

Startups recognized by DPIIT

Recognized Lenders

Foreign commercial banks, export credit agencies, international capital markets, and foreign equity holders with minimum equity stakes are eligible lenders.

End-Use Restrictions and Permitted Uses

Permitted End Uses

Infrastructure development (roads, ports, power)

Manufacturing and capital expenditure

Refinancing existing ECBs

Overseas acquisitions or modernization

Prohibited Uses

On-lending for investment in capital markets

Real estate activities (except affordable housing)

General working capital or repayment of domestic loans

Currency, Tenor, and Interest Rate Regulations

Currencies: USD, Euro, Yen, or INR (for Track III).

Tenor: Minimum 3 years for Track I; 10 years for Track II.

All-in-Cost Ceiling: Benchmark rate (SOFR, EURIBOR, etc.) + 450 basis points.

These ensure transparency and alignment with global benchmarks.

Advantages of External Commercial Borrowings

Lower Cost of Funds: Global interest rates are often more favorable than Indian lending rates.

Longer Tenor: ECBs provide medium-to-long-term funding options.

Diversified Financing Sources: Reduces dependency on domestic banks.

Boost to Infrastructure and Growth: Ideal for capital-intensive projects.

Risks and Challenges

Exchange Rate Volatility: Depreciation of the rupee increases repayment burden.

Regulatory Complexity: RBI and FEMA compliance can be extensive.

External Market Risks: Dependence on foreign economic conditions and credit ratings.

ECB Process Flow – Step-by-Step Overview

Eligibility Check – Confirm borrower and lender criteria.

Loan Negotiation – Define terms and conditions.

Form ECB Submission – File with RBI within 7 days of drawdown.

Drawdown & Utilization – Funds used only for permitted activities.

Repayment & Reporting – Regular updates via monthly ECB-2 returns.

Impact of ECBs on India’s Financial System

Encourages private sector participation in national development.

Strengthens India’s foreign exchange reserves.

Contributes to sustainable infrastructure financing.

Recent RBI Updates (2024–2025)

ECB limits increased for startups and NBFCs.

RBI relaxed hedging norms for long-term infrastructure loans.

Encouragement of ESG-linked and sustainability bonds under ECB framework.

Comparison: ECBs vs Domestic Borrowing

Parameter | ECBs | Domestic Borrowing |

|---|---|---|

| Cost of Capital | Lower (global rates) | Higher (repo-linked) |

| Regulation | RBI & FEMA | RBI & Indian Banks |

| Currency Risk | Yes | No |

| Tenor | Medium to Long | Short to Medium |

| Ideal For | Infrastructure, CapEx | Working Capital |

Future Outlook for ECBs in India

As India advances toward becoming a $5 trillion economy, ECBs will continue to serve as a critical channel for foreign capital inflow.

Emerging trends include:

ESG-linked ECBs for sustainable development

Fintech platforms simplifying global borrowing

Hybrid ECB models combining foreign and domestic capital sources

FAQs on External Commercial Borrowings (ECBs) in India

Q1. What are ECBs?

Loans raised by Indian entities from foreign lenders for permitted uses under RBI and FEMA guidelines.

Q2. Who regulates ECBs?

The Reserve Bank of India (RBI).

Q3. What is the difference between Automatic and Approval Route?

The Automatic Route needs no prior RBI approval; the Approval Route does.

Q4. Can startups raise ECBs?

Yes, recognized startups can raise ECBs up to USD 3 million annually.

Q5. What are the key risks of ECBs?

Currency risk, regulatory compliance, and global interest rate fluctuations.

Q6. What is the minimum maturity for ECBs?

3 years under Track I and 10 years under Track II.

Conclusion – The Road Ahead for Global Borrowing in India

External Commercial Borrowings continue to be a vital financing tool for India’s growth story. With prudent regulation, diversified funding access, and global investor interest, ECBs help Indian enterprises scale up and compete internationally — while reinforcing India’s position as an attractive investment destination.

For detailed RBI guidelines, visit: Reserve Bank of India – Master Direction on ECBs