What is Promoter’s Funding?

Promoter’s Funding is a financing option where company promoters raise money by pledging their shares as collateral. Instead of selling equity or taking a traditional loan, promoters use their ownership stake to access short- or medium-term funds.

This approach is common in India for expansion, refinancing, or working capital needs. Unlike private equity, it allows promoters to retain control and ownership of their company.

Why Promoter’s Funding Matters in India

Supports growth

→ Enables expansion into new markets or projects.Provides liquidity

→ Useful during cash flow shortages or emergencies.Builds investor confidence

→ Shows promoters’ commitment to their own company.

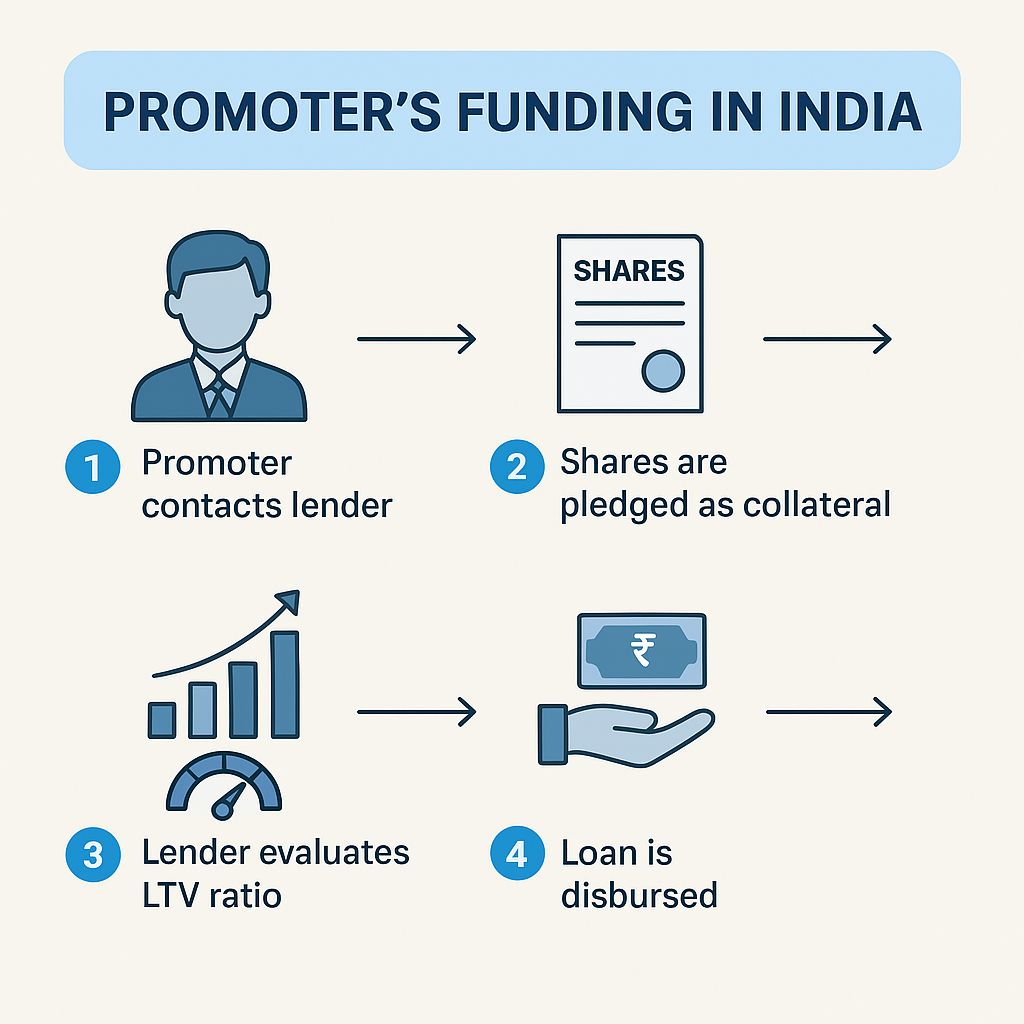

How Promoter’s Funding Works

- Promoter contacts a bank, NBFC, or financial institution.

- Shares are pledged as collateral.

- The lender checks the Loan-to-Value (LTV) ratio, usually 40–60%.

- Loan is disbursed quickly.

- Once repayment is complete, shares are released back to the promoter.

👉 Example: A Mumbai-based promoter pledges shares worth ₹100 crore and secures a ₹45 crore loan to fund a real estate project.

Types of Promoter’s Funding in India

Loan Against Shares

→ Classic funding backed by pledged shares.Loan Against Promoter’s Holding

→ Structured finance for large listed companies.Customized Promoter Financing

→ Tailored solutions for big corporates via investment banks.

Advantages of Promoter’s Funding

- Quick access to funds without waiting months for equity investments.

- Retains promoter’s control in the company.

- Flexible end-use for expansion, acquisitions, or refinancing.

Risks and Challenges

Market dependency

→ Falling share prices may trigger margin calls.

High interest rates

→ Typically higher than business loans.

Ownership risk

→ Default may lead to lenders selling pledged shares.

Promoter’s Funding vs Private Equity

Factor |

Promoter’s Funding |

Private Equity |

| Ownership | Retained by promoter | Diluted |

| Cost | Loan interest only | Higher, with profit sharing |

| Control | Full control retained | Investors influence decisions |

| Speed | Quick access | Slow due to due diligence |

Eligibility for Promoter’s Funding

- Promoter must hold a significant shareholding.

- Shares should be listed and actively traded.

- Strong credit history improves approval chances.

Where to Get Promoter’s Funding in India

Banks & NBFCs

→ ICICI Bank, HDFC, Bajaj Finance, Edelweiss.

Investment Banks

→ Structured deals for large corporates.

Fintech Platforms

→ Fast approvals and digital processes.

Alternatives to Promoter’s Funding

Rights Issue

→ Promoters and investors buy more shares.Private Placement

→ Selling shares to select investors.Traditional Loans

→ Asset-backed loans from banks.

Best Practices for Promoters

- Avoid over-leverage to reduce risk.

- Balance debt and equity financing.

- Maintain transparency with lenders.

Case Studies

Real Estate

→ NCR and Mumbai developers use promoter funding to launch projects.Startups

→ Founders pledge shares for interim funds before big funding rounds.Manufacturing

→ Auto and textile promoters raise capital to modernize plants.

Future of Promoter’s Funding in India

NBFC growth

→ Non-banking firms expanding loan products.

Digital solutions

→ Faster disbursals via fintech platforms.

SEBI regulations

→ Stricter disclosure norms increase investor confidence.

FAQs on Promoter’s Funding

1. What is promoter’s funding?

It’s financing raised by pledging promoter’s shares as collateral.

2. Is it safe?

Who provides bridge funding in India?

Yes, but risks exist if share prices fall or repayment is delayed.

3. Who provides promoter funding in India?

Banks, NBFCs, and investment banks.

4. What’s the typical interest rate?

Usually between 12–18% annually

5. Can unlisted companies avail it?

Mostly for listed firms, since shares need market liquidity

6. How is it different from private equity?

Promoter’s funding retains control, while private equity dilutes ownership.

Conclusion

Promoter’s Funding in India is a powerful financing tool for businesses seeking quick capital without losing ownership. It’s especially useful for real estate, startups, and manufacturing sectors. While it carries risks like high interest rates and market dependency, the benefits of liquidity and control make it an attractive option.

👉 For more details, visit RBI or SEBI.

👉 Explore related financing methods like Bridge Funding in India.