India’s evolving financial ecosystem has paved the way for innovative financing mechanisms. Among these, Structured Finance stands out as a strategic tool that bridges the gap between traditional lending and complex capital market solutions.

In simple terms, Structured Finance in India refers to tailor-made financial instruments that help companies raise large-scale funds, manage risks, and optimize their balance sheets. It’s especially popular among NBFCs, banks, and corporations dealing with long-term infrastructure, real estate, or asset-heavy projects.

As India pushes toward becoming a $5 trillion economy, structured finance plays a crucial role in supporting credit expansion, infrastructure funding, and financial inclusion.

What is Structured Finance?

Definition and Core Concept

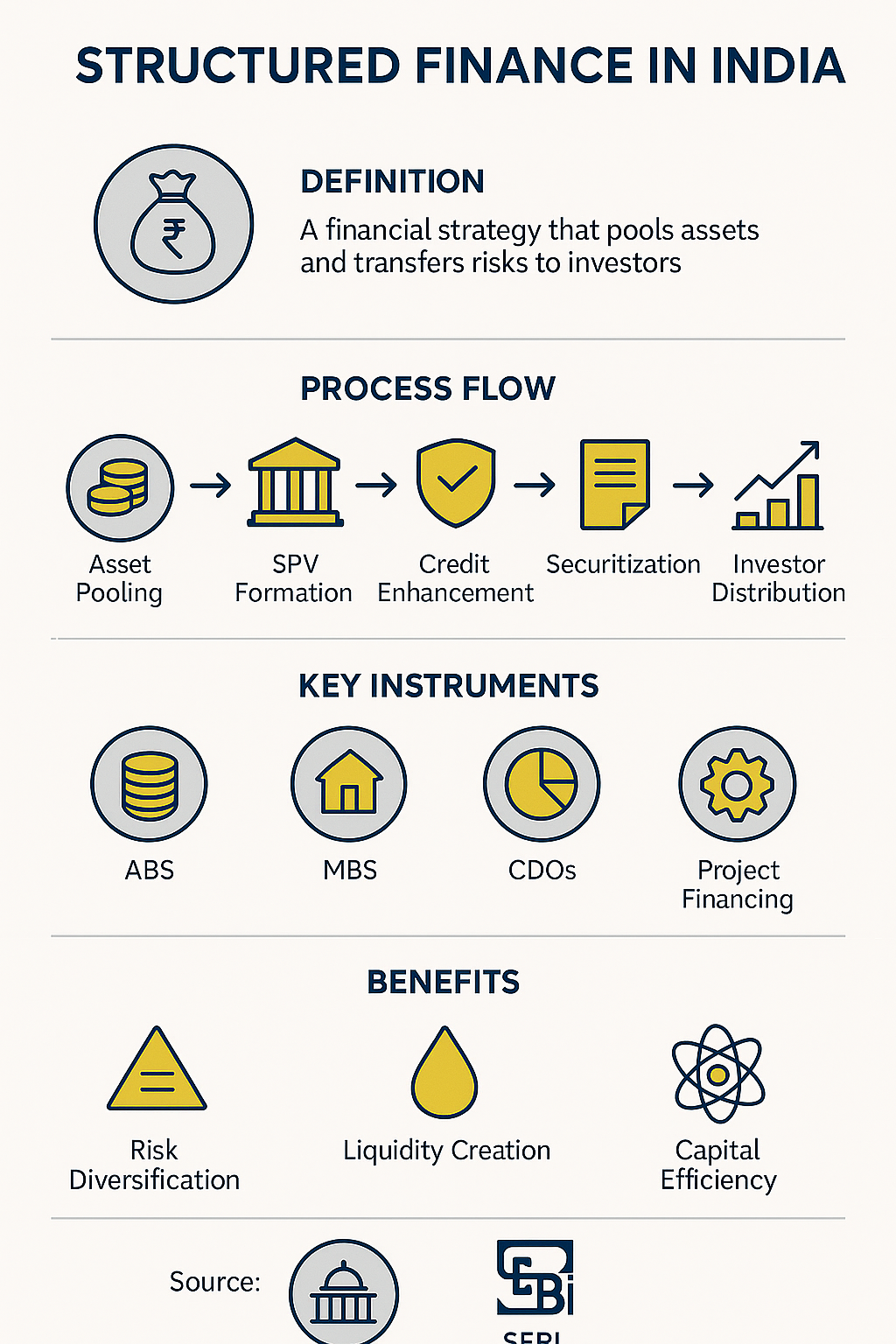

Structured finance is a form of non-traditional financing designed to meet unique funding needs that cannot be solved with conventional loans. It involves pooling financial assets and creating financial securities that are then sold to investors.

This approach helps in spreading risk and freeing up liquidity for lenders.

How Structured Finance Differs from Traditional Finance

Aspect

Traditional Finance

Structured Finance

Source of Capital

Direct bank lending

Capital market investors

Risk Distribution

Concentrated with the lender

Distributed among investors

Flexibility

Standardized

Customized for specific needs

Examples

Loans, overdrafts

ABS, MBS, CDOs, SPVs

Importance of Structured Finance in India

Supporting Corporate Growth

Structured finance allows Indian corporations to raise large-scale funding without diluting equity. By using structured instruments, companies can unlock cash flows from existing assets and fund expansion or new ventures.

Risk Mitigation and Liquidity Creation

By transferring financial risks to capital market investors, structured finance reduces concentration risks and improves liquidity—critical for NBFCs and banks under regulatory pressure.

Role in Infrastructure and Real Estate

Structured finance has become a key funding channel for India’s infrastructure and real estate sectors, where traditional financing is often inadequate due to long gestation periods and regulatory hurdles.

Key Instruments of Structured Finance

Asset-Backed Securities (ABS)

ABS are financial securities backed by income-generating assets like loans or leases. In India, NBFCs frequently use ABS to securitize vehicle loans, microfinance receivables, and SME loans.

Mortgage-Backed Securities (MBS)

MBS are backed by home loans. Housing finance companies like HDFC and LIC Housing Finance use MBS structures to access liquidity and lower funding costs.

Collateralized Debt Obligations (CDOs)

CDOs are complex instruments backed by diversified debt pools, offering investors tiered risk and return options.

Securitization Transactions

These involve converting illiquid assets into tradable securities, providing liquidity and capital relief for financial institutions.

How Structured Finance Works

Pooling of Financial Assets

Assets like loans, leases, or receivables are pooled together to create a diversified investment product.

Role of Special Purpose Vehicles (SPVs)

An SPV is created to isolate financial risk and issue securities backed by the pooled assets.

Credit Enhancement Techniques

Guarantees, over-collateralization, or insurance are used to improve the credit quality of structured products.

Distribution to Investors

The securities are sold to institutional investors, who earn returns from cash flows generated by the underlying assets.

Types of Structured Finance in India

Corporate Structured Debt

Tailored financing solutions for large corporations, often used for mergers, acquisitions, or leveraged buyouts.

Project Financing

Used in long-term infrastructure projects like highways, power plants, and airports.

Lease and Receivable Financing

Allows businesses to unlock working capital from future receivables or lease contracts.

Securitization by NBFCs

NBFCs use structured finance to sell their loan portfolios to banks or funds, creating liquidity and risk diversification.

Benefits of Structured Finance

Diversification of Risk: Distributes credit risk among investors.

Capital Efficiency: Frees up regulatory capital for lenders.

Access to Alternate Capital Sources: Taps into global and domestic investors.

Liquidity Creation: Converts illiquid assets into tradeable securities.

Risks & Challenges in Structured Finance

Complexity in Structuring Deals

The instruments require financial engineering expertise, which can increase transaction costs.

Regulatory Oversight and Compliance

Complex documentation and changing RBI/SEBI regulations demand robust governance.

Credit Risk and Market Volatility

Economic downturns can impact asset performance, affecting investor returns.

Structured Finance Regulations in India

Role of RBI and SEBI

Both regulators monitor securitization transactions and investor protection norms.

Guidelines on Securitization and SPVs

RBI’s 2021 framework governs risk retention, due diligence, and transparency in structured deals.

Basel Norms and Indian Banking Practices

Structured products must align with global Basel III standards to manage systemic risk.

Used for refinancing completed infrastructure projects with predictable cash flows.

NBFC Securitization Trends

Post-IL&FS crisis, securitization provided NBFCs with much-needed liquidity.

Housing Finance Securitization

Enabled mortgage lenders to recycle funds for affordable housing projects.

Future of Structured Finance in India

Digital Securitization Platforms

Fintech-driven platforms are automating securitization, improving transparency.

Green and ESG-Linked Structured Products

Sustainability-linked bonds and green ABS are gaining traction among investors.

Role of Fintech and AI in Credit Structuring

AI models are being used for credit scoring, risk analysis, and portfolio optimization.

FAQs on Structured Finance in India

1. What is the meaning of structured finance in India?

Structured finance refers to customized financial arrangements that use asset pooling and securitization to raise funds efficiently.

2. How does structured finance differ from regular loans?

Unlike traditional loans, structured finance involves transferring risk to investors via market-based instruments.

3. Who regulates structured finance in India?

The Reserve Bank of India (RBI) and the Securities and Exchange Board of India (SEBI) oversee structured finance transactions.

4. Which industries benefit most from structured finance?

Infrastructure, real estate, NBFCs, and housing finance companies are major beneficiaries.

5. What are the risks associated with structured finance?

Market volatility, credit defaults, and regulatory complexities are primary risks.

6. Is structured finance suitable for small businesses?

While primarily used by large corporations, fintech platforms are making structured finance accessible to SMEs.

Conclusion – Why Structured Finance Matters for India’s Growth

Structured Finance in India is no longer limited to large corporations; it’s emerging as a catalyst for financial innovation and inclusion. With RBI’s proactive regulation, fintech integration, and investor appetite for diversified risk products, structured finance will remain vital to India’s journey toward sustainable growth.